Frequently Asked Questions

- What is a Life Settlement?

- Why do people sell their insurance policy?

- Why consider this as an investment?

- How does the seller benefit?

- How does an Insured find out how much their policy is worth?

- How large is the available pool of policies?

- Who is Investing in Life Settlements?

- What makes this opportunity exist?

- What constitutes a qualifying policy?

- What is AIM?

-

What is a Life Settlement?A Life Settlement provides a lump sum cash payment to an insurance policy-holder in exchange for contract ownership rights. The Acquisition cost is based on a fraction of the policy's face value and exceeds the policy's surrender value available to the policy owner. The new owner assumes responsibility for payments to keep policy in force throughout the life of the insured. Life Settlements are similar to a negative-coupon long bond, with an indefinite maturity.

Life insurance policies are generally purchased from individuals who are over the age of 65 and have remaining life expectancies between four and twelve years (although in some cases, life expectancies outside this range will be considered).

Back to Top -

Why do people sell their insurance policy?There are a variety of reasons people may seek to sell their life insurance policy. For example:

- Premiums may have become unaffordable and the policy is in danger of lapse;

- Estate-planning needs of the insured may have changed significantly;

- Funds might be needed for long-term health care;

- When the designated beneficiary has changed because of death or divorce;

- As a business decision in the disposal of unneeded business-owned insurance, such as "key-man" insurance;

- To fund new annuities, life insurance, or investments;

- To satisfy the need for cash in a forced liquidation due to bankruptcy or other financial difficulties;

- As a liquidation of policies donated to not-for-profits;

- As a way to dispose of policies that are no longer needed or wanted.

Back to Top -

Why consider this as an investment?Life Settlements are one of several life insurance practices, that make it possible to realize profits through innovative actuarial analyses and careful assessment of mortality and other risks.

The emerged sales of Life Settlement policies have created a secondary marketplace for existing life insurance policies. The buyer of the policy becomes the policy's owner and beneficiary, as well as a payer of future premiums. The buyer, having taken over payments of the premiums, collects full proceeds of the life insurance policy upon death of the insured.

Back to Top -

How does the seller benefit?The percentage of the policy's face value that is provided to the seller is based upon sophisticated underwriting models that allow the purchase of policies from individuals who are not terminally ill, yet may typically provide them a cash payout ranging from 15% to 50%, depending upon the life expectancy, health history, and premium obligation the buyer will assume over the life expectancy of the insured.

For the insured, Life Settlements help address a variety of financial planning concerns - from meeting estate tax needs to protecting against various individual and business risks. When circumstances change, policyholders may not be able, wish, or need to continue paying premiums to maintain their policies. Changes of circumstances arise from events, such as retirement, health problems, divorce, fluctuation in estate size, and the sale of a business or it may be that the policy holder wishes to use the money to make other investments. When these events occur, the option of a Life Settlement contract should be evaluated. It is possible that the policy owner's present-day objectives can better be accomplished by selling the policy.

Back to Top -

How does an Insured find out how much their policy is worth?Unlike a life insurance application, no medical examination is required. The Insured would simply complete an application that provides information on the life insurance policy, and provide the most recent medical records along with a current HIPAA release form. The Insured can contact Seven Hills Settlements for suggestions on how to find a broker that can assist through this process.

Back to Top -

How large is the available pool of policies?Recent estimates indicate that the potential market for Life Settlements is close to $100 billion. Seven Hills Settlements maintains standards that enable various kinds of life insurance policies to be considered for a Life Settlement, including term, whole-life, universal, survivorship, and variable life insurance policies. The policy can be owned individually, by a partnership or corporation, or by a trust. It must be beyond the "contestability" period of the insurer, and must be issued by a carrier rated "A-" or better by Standard & Poor's, or an equivalent rating by other major agencies.

Life Settlements are a logical growth of the life insurance industry that provides a needed secondary market for insurance policies. Modeling what has already happened to real estate and equity markets, as more policyholders become aware of the opportunities presented by Life Settlements, and as it becomes possible for more policyholders to obtain the fair value of their policies, consumers perceive an improvement in the quality of life insurance industry in general. This, in turn, has a positive effect on the demand for life insurance and for Life Settlement transactions.

More than twenty percent of policyholders over the age of 65 are estimated to hold policies with economic values exceeding their cash surrender values. Life Settlement sales constituted $2.2 billion in 2002 and are expected to reach $20 billion per year in the next ten years. This is due mainly to the increase in the senior population and, consequently, the amount of available insurance held by that population. It is estimated that the total value of life insurance policies owned by senior citizens is $492 billion - indicating a potential market for eligible Life Settlements that is close to $100 billion. This number does not include corporate "key person" or trust-owned policies insuring individuals of 65 years of age or older. Life Settlement companies estimate an additional $200 billion of in-force coverage from these sources. Given the relative infancy of the Life Settlement industry, it can be anticipated that, as it matures, qualified Life Settlements will become available in even greater numbers.

Back to Top -

Who is Investing in Life Settlements?Life Settlements interests both private and institutional investors:

- Retail Funds (in the UK, Germany, Latin America, and Asia)

- Insurance Companies

- Hedge Funds

- Pension Funds

- Family Offices

- Banks

Back to Top -

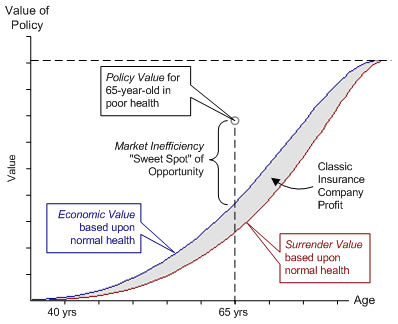

What makes this opportunity exist?This is best demonstrated in an example:

Assume that a policyholder buys a whole-life policy at age 40. The buildup of policy value demonstrated here is based on the assumption that the policyholder's health follows a normal pattern as he ages. The vertical distance between the two curves represents the economic margin earned by the life insurance carrier on the surrender of a healthy policy, together with an allowance for transaction costs.

If the policyholder's health suddenly deteriorates at age 65, the actuarial value of the policy will be much higher than for a 65-year-old in normal health. Life insurance carriers do not offer health-adjusted surrender values because pricing difficulties outweigh the benefits they might obtain by offering them to customers. This market inefficiency has created a lucrative "sweet spot" of opportunity to purchase impaired policies at competitive rates that should yield high returns. As a result, policy owners who desire to sell their life insurance contracts, provide buyers the opportunity to obtain attractive returns on investment.

Back to Top -

What constitutes a qualifying policy?Seven Hills Settlements facilitates the purchase of Life Settlement policies of individuals who are over the age of 65 and have remaining life expectancies of between four and twelve years (although in some cases life expectancies outside of this range are considered). To meet prerequisites for policy selection, the policyholder must:

- be able to provide evidence of mental competency, and voluntary and knowing consent to sell the life insurance instrument;

- be willing and able to provide all necessary documentation required by the assessing company;

- be a resident of and residing in the United States of America;

- not be subject to any receivership, insolvency, domestic relations or divorce proceedings, or bankruptcy proceedings; and

- not be an employee of the Seven Hills Settlements or affiliates.

Back to Top -

What is AIM?Seven Hills Settlements employs a four-phase proprietary Acquisition of Insurance Methodology (AIM) to effectively and efficiently obtain and manage Life Settlement policies. This methodology includes extensive computer-assisted administrative and client information database functions based upon bifurcated medical evaluation techniques that blend medical information with actuarial data. Policies and processes applied within AIM can be summarized in the following workflow:

1. Origination. Associated brokers and agents submit potential policies for review and analysis. This is a preliminary function that allows an initial review of available product.

2. Evaluation. An actuarial analysis is conducted to verify that the candidate meets Life Expectancy (LE) requirements and that the policy is within the guidelines established by Seven Hills Settlements. It is performed in three functional areas:

a. Medical: Medical records of the insured are requested. They are forwarded to evaluating agencies and medical professionals who provide medical evaluation and morbidity assessments, usually within two to five working days. These reports are reviewed and may be subject to further discussion with consulting physicians.

b. Insurance: During the same period, Verification of Coverage is conducted to ensure that the policy meets all necessary criteria. From this, the Cost of Insurance (COI) is determined.

c. Financial: A proprietary valuation pro forma model is used to ascertain the asset value of the instrument for the portfolio, as well as to determine projected costs and the rate of return. The model components and variables include: (i) amount of death benefit (i.e., the policy face amount); (ii) nominal maintenance fees to be charged; (iii) an acquisition fee generally equal to 1% of the policy face amount; (iv) insurance premiums to be paid over the expected life of the insured; and (v) documented life expectancy (LE).

3. Acquisition. Qualifying policies enter into a bid process for acquisition. All submissions that have not been approved are archived in accordance with applicable HIPAA requirements and the management's needs of Seven Hills Settlements.

4. Management. Policies that have been obtained are placed in a portfolio to be ultimately maintained to maturity by the Management Company. This strategy does not allow any one single Life Settlement policy to have more importance than another.

Back to Top